Financial Statement is document showing the clear picture of business & the information provided in the financial statements helps investors to understand the company or organization doing well or not? By reading the financial statements investors can be able to conclude that whether the company is prepared for any unforeseen conditions / crisis in future.

Financial Statements consist of three main statements:

- Balance Sheet

- Profit and Loss Statement

- Cash Flow Statement

In this article we are going to discuss about the Balance Sheet and in the upcoming articles we will discuss about the other two statements.

Money is the key element for every business so Money can be termed as a Oxygen for survival of a business of a company or an organization. Balance sheet is the most important & crucial document in of a financial statement and contains all financial aspects of a company and is a vital document that an investor must know how to crack the information from the Balance Sheet.

What is a Balance Sheet?

The term balance sheet refers to a financial statement that reports company’s assets, liabilities and shareholder’s equity at specific point of time. Balance sheet provides the basis for computing rates of return for investors and evaluating company’s capital structure. In short the balance sheet is a financial statement that provides a snapshot of what the company owns and owes as well as the amount invested by the shareholders.

Balance sheet study put together with other financial statements is the basis for fundamental analysis of the company and helps in calculating the important financial ratios.

The Balance sheet accounting equation consists of assets on one side and liabilities plus share holders equity on the other side.

Assets = Liabilities + Shareholders.

Balance Sheet is the financial statement of a company which includes assets, liabilities, equity capital, total debt, etc. at a point in time. Balance sheet includes assets on one side, and liabilities on the other. For the balance sheet to reflect the true picture, both heads (liabilities & assets) should tally (Assets = Liabilities + Equity).

So to summaries with key points to remember are listed below

- A balance sheet is a financial statement that reports a company’s assets, liabilities, and shareholder equity.

- The balance sheet is one of the three core financial statements that are used to evaluate a business.

- It provides a snapshot of a company’s finances (what it owns and owes) as of the date of publication.

- The balance sheet adheres to an equation that equates assets with the sum of liabilities and shareholder equity.

- Fundamental analysts use balance sheets to calculate financial ratios.

Understanding the 3 Elements of Balance Sheet :

Assets

Accounts within this segment are listed from top to bottom in order of their liquidity. This is the ease with which they can be converted into cash. They are divided into current assets, which can be converted to cash in one year or less; and non-current or long-term assets, which cannot.

General Layout of accounts within current assets:

- Cash and Cash Equivalents are the most liquid assets and can include Treasury bills and short-term certificates of deposit, as well as hard currency.

- Marketable Securities are equity and debt securities for which there is a liquid market.

- Account Receivable (AR) refer to money that customers owe the company. This may include an allowance for doubtful accounts as some customers may not pay what they owe.

- Inventory refers to any goods available for sale, valued at the lower of the cost or market price.

- Prepaid expenses represent the value that has already been paid for, such as insurance, advertising contracts, or rent.

Long-term assets include the following:

- Long-term investments are securities that will not or cannot be liquidated in the next year.

- Fixed Assets include land, machinery, equipment, buildings, and other durable, generally capital-intensive assets.

- Intangible assets include non-physical (but still valuable) assets such as intellectual property and goodwill. These assets are generally only listed on the balance sheet if they are acquired, rather than developed in-house. Their value may thus be wildly understated (by not including a globally recognized logo, for example) or just as wildly overstated.

Liabilities

A liability is any money that a company owes to outside parties, from bills it has to pay to suppliers to interest on bonds issued to creditors to rent, utilities and salaries. Current liabilities are due within one year and are listed in order of their due date. Long-term liabilities, on the other hand, are due at any point after one year.

Current Liabilities accounts might include:

- current portion of long-term debt

- bank indebtedness

- interest payable

- wages payable

- customer prepayments

- dividends payable and others

- earned and unearned premiums

- accounts payable

Long Term Liabilities can include:

- Long Term Debt includes any interest and principal on bonds issued

- Pension fund liability refers to the money a company is required to pay into its employees’ retirement accounts

- Deferred Tax Liabilities is the amount of taxes that accrued but will not be paid for another year. Besides timing, this figure reconciles differences between requirements for financial reporting and the way tax is assessed, such as depreciation calculations.

Some liabilities are considered off the balance sheet, meaning they do not appear on the balance sheet.

Shareholder Equity

Shareholders Equity is the money attributable to the owners of a business or its shareholders. It is also known as net assets since it is equivalent to the total assets of a company minus its liabilities or the debt it owes to non-shareholders.

Retained earnings are the net earnings a company either reinvests in the business or uses to pay off debt. The remaining amount is distributed to shareholders in the form of dividends.

Treasury stock is the stock a company has repurchased. It can be sold at a later date to raise cash or reserved to repel a hostile takeover.

Some companies issue preferred stock, which will be listed separately from common stock under this section. Preferred stock is assigned an arbitrary par value (as is common stock, in some cases) that has no bearing on the market value of the shares. The common stock and preferred stock accounts are calculated by multiplying the par value by the number of shares issued.

Additional paid-in capital or capital surplus represents the amount shareholders have invested in excess of the common or preferred stock accounts, which are based on par value rather than market price. Shareholder equity is not directly related to a company’s market capitalization. The latter is based on the current price of a stock, while paid-in capital is the sum of the equity that has been purchased at any price.

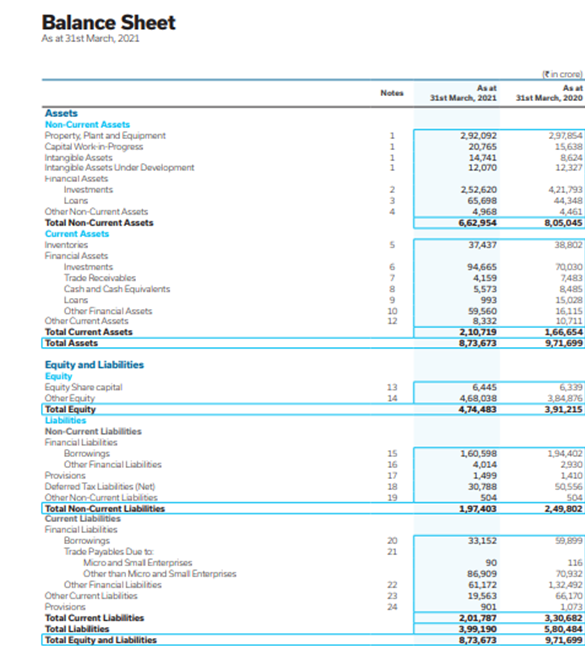

So for more clarity you can go through the balance sheet enclosed below of reliance industries.